The risks are multiplying; will global supply chains become obsolete?

30 juni 2020

This exploratory article examines the formulation of a business case to compare production near-shoring with off-shoring and examines the risks of single sourcing. It further lays out the implications this may embody for future supply chains.

A transitory promise

The economic entry of China and the so-called Asian tigers into the global market during the 1990s quickly led to an exodus of production facilities from particularly Europe and North America. Through either owned or outsourced production resources, this move provided excellent opportunities to take advantage of very attractive labor and investment costs while reduced regulatory control provided further impetus to the decision making1.

Low shipping and handling costs also ensured that the ensuing logistics handling of freight transport proved beneficial. With the apparel industry at the helm, off-shoring became booming business. The collection of interested parties continued growing while there seemed to be no end to willing Asian counterparts to conduct business with. As early as 2009, China surpassed production output from countries like the US, Germany and Japan2, and if the competition takes advantage of such attractive offerings, no one wants to stay behind.

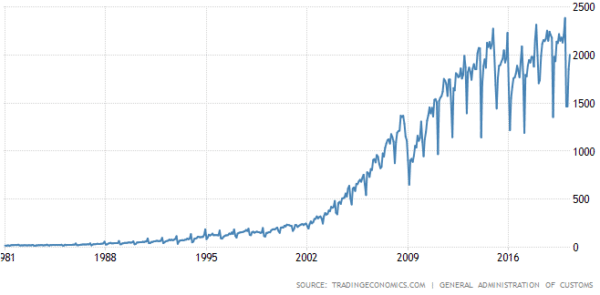

CHINESE EXPORTS IN Bn USD, 1981-2020 (tradingeconomics.com/china/exports)

The past 5 years have seen economic developments in particularly China to be less than prosperous3. Labor costs have risen sharply in recent years and the population is rapidly aging without renewal being on equal footing, placing pressure on future labor cost developments. The IMO2020 regulations issued by the International Maritime Organisation have become effective as of January this year, outlining further restrictions on CO2 and sulfur emissions in shipping4. The most innovative element used by shipping companies to meet these requirements, so-called scrubbers, can be installed as an add-on to the vessel’s engines to act as an exhaust cleaning system at an investment of several million euros per ship5. Besides the positive elements this anti-pollution mandate wishes to pursue, the negative impacts on increased operating costs will be transferred to customers via increased freight rates. Another resultant is expected in the reduction of global fleet capacity as older ships will likely now be taken out of service at an accelerated pace, over and above an already existing desire for greener and more sustainable port facilities that will contribute further to investments passed on to shipping companies, and therefore indirectly to what their clients will be charged with6. In viewing global shipping from a long term perspective, it is as yet uncertain what the recent developments in China – US trade relations and consequent price volatility will bring, but it has been shown to exist and may also disrupt trade relations in other parts of the world. Producing in China was initiated with the intent to market large quantities of standardized products, and it appears that today’s customers have a higher appetite for customized products. The cost structure of offshoring was never set up for that purpose, and already in some cases, it is now possible to produce cheaper in Europe than it is in China7.

Single source of origin

Whether or not developed hand in hand with offshoring, the same era also witnessed a greater emphasis on cost saving through production scale up via single-sourcing. The cost benefits compared to the alternative variant called multi-sourcing were significant as they do not only result in lower unit production costs from economies of scale, but it also resulted in having to maintain a much more simplified supply chain set up that can function with considerably lower operating costs in the single-sourcing option. Over time, it has become clear that an over-reliance on one supplier (as we have seen, also at great distance) can have a greater impact on a company’s survival chances than we had until recently wanted to believe: the Corona crisis has more than laid bare the negative consequences of single-sourcing with the centralising of medical devices and equipment like mouth mask production in China. Likewise, the legitimacy of many organizations is now jeopardised by the same single-source decisions that seemed completely sensible in the not too distant past. The world is currently undergoing a pandemic that may have been caused by an infected bat that someone thought looked appetizing. And although opinions may differ about the actual cause; the fact remains that the natural origins of this disruption fell well outside the perception of those who have written libraries full about risk mitigation in global supply chains. The question is therefore what other unknown risks can disrupt those chains. What will the books in those libraries have to say about the economic crisis that is now developing as a result of this pandemic? How shall we mitigate that? There are no scenarios to mitigate this crisis and unlike business continuity plans, I have never heard of a ‘society continuity plan’, based for instance on a strategy whereby governments may place regulations on the production of society-critical supplies. Because of these ‘unknown unknowns’, blended in with already known risks, isn’t it wiser nowadays to opt for reduced risks and more manageable, resilient supply chains rather than letting them be subjected to uncontrollable and unforeseen risks?

Business case

Pre-Corona, it was already well-known that due to aspects such as rising Asian wage and transport costs, the long shipping distances and associated environmental pollution, the lack of control and chain visibility, and the mitigation of logistics risks and supply chain sustainability, internationally operating companies should rethink their sourcing and supply chain strategies. Those topics are now made urgent by the burning platform caused by the Corona crisis we are currently going through, and this platform also includes a possible next Corona outbreak in the near future. Additionally, a host of additional disaster scenarios have emerged as a result of global warming that will further put global supply chains at risk8. The effects of the recent shortages in critical medical goods, masks and other Corona protective equipment to name one example, breathing machines being another, have clearly demonstrated the social consequences of one-sidedly cost-based supply chain decisions. Such myopic attitudes in appropriately assessing supply chain risks will increasingly threaten a company’s long term existence in any industry and therefore these risks must play a fundamental role in the shaping of current and future strategic supply chain decisions. A business case underlying those risk appraisals will include valuation of the above aspects to be compared with the pros and cons of alternative scenarios. One such scenario is the nearshoring or reshoring of production facilities closer to the sales market9.

Insight into this business case is gained by first realising that we are dealing with a threefold problem, formulated as follows: How can we price-consciously produce the same product closer to home and also avoid over-reliance on one supplier, while additionally taking into account sustainability aspects that currently apply or may play a role in the near future, or may even be imposed? With this statement, we recognize to not only wanting to shorten lead times and keep costs under control, but also want to reduce the risks associated to single-sourcing and the desire to establish a much more sustainable supply chain.

Lead times

Near-shoring implies the reducing of shipping lead times which enables a positive impact on product availability. Response times to the market are shortened and this opens the way to smaller batch size production, which in turn is beneficial to the overall supply chain flexibility.

By reducing transport distances we also find that response times to erratic, rapidly changing consumer demand patterns are considerably reduced. Stock obsolescence is prevented and thus do not have to be discarded, the depreciation of which also weighs heavily on the operating result. Lead time reduction further means that capital invested in inventory is freed up for other purposes.

Cost control

The off-shoring exodus to China during the 1990s was triggered by sharp declines in deep-sea shipping rates10 aside from the discovery that Asian labor costs were considerably lower than in Western production countries. Now that Chinese labor costs are starting to increase to the levels of European and North-American (peripheral) regions11, the search for alternatives is increasing. This exploration is mainly focused on other Asian countries such as Vietnam, Cambodia and the Philippines where, stimulated by further lowered wages, especially production of low-cost items is being moved from China12. This will lead to shipping costs having a higher relative contribution to the total landed product costs. Given the developments of the 4th industrial revolution, marked by extraordinary technology-driven advances, the benefits of innovative automation solutions should be captured to enable remarkable savings in shipping as well. Methods like 3D-printing and robotisation offer highly innovative and useful production options that can be established closer to home. The search for new production locations should thus not only be limited to a geographic area that may fit best to immediate corporate-economic concerns, but should incorporate the longer term benefits of production automation. When applied, near-shoring then not only entails a reduction in both transport and labor costs, but can also alleviate labor market dependence, thereby providing an answer to the question where affordable staff can still be found in a shrinking global labor market.

When looking at locations for cost-conscious and efficient near-shoring, our European eye quickly falls on countries in Eastern Europe, Southern Europe and Turkey. In all three of these areas, freight transport within Europe provides cost-effective and efficient options in terms of time, distances and costs when compared to deep-sea shipping, with inland waterways and rail transport preferred over road in terms of cost and sustainability13.

Supply chain innovations in the form of electric and hydrogen-powered trucks and concepts such as truck sharing are on the rise. Multi-modal transport setups offer opportunities to operate both cost-consciously and sustainably. A precondition for such integration must be that chain visibility and good planning options are present in the form of thorough S&OP planning for supply and demand coordination across the supply chain and transport control for trunking, coordination of multi-modal operations and last-mile deliveries. This level of control is nowadays increasingly set up in the form of control towers.

Pros & Cons

Nearshoring has attracted renewed interest from major multi-nationals since 2017 in response to overseas cost increases in labor and transportation, growing regional political instability, and due to the risks that may arise from trade wars that could potentially wield tariff hikes. At the time, a 2018 McKinsey report14 discussed US nearshoring solutions in neighboring countries like Mexico, Puerto Rico and even Canada. For these organizations, the differences in total landed costs compared between nearshoring and offshoring nowadays are found to be of less importance than the strategic issue of how to serve the market as efficiently as possible, freed from supply disruptions. Elements like risk reduction and time-to-market thus play a much larger role than having a supply chain that is merely run on minimal costs. For many consumers brand loyalty no longer exist and the importance of actually having your ‘stuff on the shelves’ weighs more prominent than before to avoid customers from looking for alternatives.

One of the few drawbacks in the nearshoring vs offshoring trade-off is the labor cost argument that may be higher with nearshoring. Only a case-by-case investigation will find whether increases in labor costs in nearshoring can be partly or completely offset by reduced transport and transshipment costs plus further associated charges that play a role in offshoring; it will often depend on the product and volumes involved.

| Offshoring | Nearshoring | |

| Pros |

Relatively low labour costs Relatively low shipping costs

|

Lower shipping costs Political stability Reduced economic risks Agile responsive supply chain Focus on sustainability Cultural similarity Similar time zones Shorter distances Reduced import fees (or none) Reduced stock obsolescence Reduced stock levels

|

| Cons |

Labour cost pressure Shipping costs pressure Stock obsolescence Supply chain inflexibility Long distances Global warming risks Less care for sustainability Cultural differences Increased stock levels Different time zones Economic risks (trade wars) Import duties No view on 2nd, 3rd tier suppliers |

Increased labor costs Possibly limited supplier pool |

Multi-sourcing

Current (global) supply chains are based on a total of minimal costs, which can, in part, be ascribed to the introduction of lean production methods. Lean management was designed to eradicate anything that even remotely looks like waste, and also led to the minimising of inventory at each supply chain node to essential requirements, without redundancy. “Lean” in this context also meant far-reaching supplier rationalizations. With what we are now facing because of the Corona pandemic, it might be time for even the staunchest Lean proponents to admit that Lean supply chains only work well in stable environments that are free of unforeseen (or underestimated) supply chain risks. Covid-19 shows that single-supplier dependence has negative consequences for business continuity and that a uniquely lean-oriented supply chain no longer fits the current zeitgeist15. Earlier references have already hinted at the expectation of future disruptions, either in the form of a virus outbreak or due to the consequences of global warming – this aside from a number of well-known risk categories. It is therefore plausible that the continuation of a single-sourcing strategy will only exacerbate already existing supply chain risks. Companies will have to arm themselves by maintaining much more resilient supply chains, starting with the introduction of a broad supplier pool from where to source – as we’ve seen, preferably also closer to home or the sales market. From the outset, It should be clear that this form of sourcing will entail higher costs due to a lack of economies of scale in production, higher administrative costs and fees per product, fragmentation of transport flows and maintenance of IT and communication resources with multiple suppliers; for example when working with S&OP processes. However, the result is that the company’s raison d’être is not fundamentally affected because risks to that effect have been kept to a minimum.

Sustainability

The media regularly reports on companies needing to make more serious efforts in exercising supply chain sustainability whereby organizations should pay more attention as to how their operations affect climate change, ethical sourcing, reducing CO2 emissions, knowing where your products are made and not tolerating child or forced labor, and perhaps not doing business in or with countries that have authoritarian perspectives on even the most basic human rights. Some companies voluntarily include these considerations in their organizational philosophies, others only abide when forced to do so. Both views collectively cover only a limited part of the answer as to how we should make the world sustainable in order to combat global warming. A very large portion lies with us, the consumer17. Continued consumerism and our common drive for ‘more-for-less’ has led to a run to the bottom of the abyss in several industries to optimise production against the lowest possible costs to secure market share. We know that a company is nothing without a customer base, and if that customer base chooses to spend its money where sustainability matters, meaning also the willingness to pay more and be happy with a little less, companies will follow these routes to continue sales and secure their market shares, even where this has consequences for their supply chain strategies. Further impeding the promoting of sustainability are China’s geo-political interests and global entanglements. Quite transparently, Beijing’s ambitions point to a dominant Chinese role on the world stage, currently exemplified through rather aggressive interactions in Ladakh and in the South-Chinese Sea. By means of large-scale investments in infrastructure, Chinese political and economic influence has spread over considerable parts of Africa and Central Asia (Belt and Road Initiative) and has also reached the European external border16. Although significant steps have been taken in reducing environmental pollution and poverty reduction, China’s domestic sustainability track record leaves much to be desired in areas such as human rights, ethics and corruption in business relationships, labour conditions and environmental management18, and the question is therefore justified to what extent sustainability considerations will be included in the elaboration of these international influences, although it should likewise be noted that other superpowers currently do not necessarily score much better in this regard.

Intrinsic direction and extrinsic motivation

With a view to a future Covid-19 recurrence and expected climate change disturbances, companies looking to mitigate their supply chain risks will choose to produce closer to the market. Global supply chains may well undergo a transition to regionally oriented supply chains that on the one hand can lead to increased costs, but on the other hand offer significantly increased supply chain flexibility and resilience and enhanced certitude of organizational existence. With the prevalence of common sense, companies will pay more attention to producing multi- or dual-sourced closer to home in order to guarantee continued product availability. These intrinsically driven changes will deliver more resilient supply chains than in the case of a global supply chain, single-sourced on the other side of the world. Consumers increasingly express their preferences about the type of products they want to purchase and demand to know how and where it is produced. Driven by this extrinsic motivation, companies will opt to respond to these changes in demand. The above considerations need to be viewed in the context of the fourth industrial revolution; if the world’s production output is manufactured by robots and other types of automation, aspects such as labor costs will become less relevant and the choice of production location will be determined factors such as investment climate, environmental and distribution costs and proximity-to-market considerations. The alignment of a business case for nearshoring should represent all of these aspects in risk assessment, automation and changing consumer behavior and convert these into financial metrics so as to expose the economic sense, perhaps even necessity, of nearshoring and multi-sourcing.

Referenties

( 1) https://tradingeconomics.com/china/exports

(2) https://www.insideover.com/economy/the-consequences-of-chinese-manufacturing-migration.html

(3)https://thediplomat.com/2017/12/is-chinas-era-of-cheap-labor-really-over/; https://www.cnbc.com/2017/01/31/china-no-longer-considered-a-low-cost-sourcing-destination-survey.html;

(5) https://www.wsj.com/articles/maritime-emissions-rule-triggers-split-in-shipping-costs-11576839601

(6) https://unctad.org/en/PublicationsLibrary/rmt2019_en.pdf

(7) https://www.vck.be/nieuws/innovatief-produceren-lokt-productie-terug-naar-belgi

(8) Zorn, M. (2018), Natural Disasters and Less Developed Countries. Nature, Tourism and Ethnicity as Drivers of (De)Marginalization, pp.59-78; https://www.un.org/development/desa/dpad/wp-content/uploads/sites/45/publication/CDP-bp-2012-15.pdf

(9) https://www.youtube.com/watch?v=JqsDgEl1Bbc (Professor Richard Wilding-Cranfield University); http://textilefocus.com/nearshoring-apparel-manufacturing-coming-home/; https://www.supplychaindive.com/news/apparel-nearshoring-cut-lead-times-McKinsey/539787/;

(10) https://ec.europa.eu/competition/consultations/2018_consortia/haralambides_annex.pdf

(11) https://www.bcg.com/documents/file84471.pdf; https://finshots.in/archive/made-in-china-no-more; https://www.industryweek.com/the-economy/article/21957116/the-end-of-cheap-china-a-review

(16) https://www.spoorpro.nl/goederenvervoer/2019/12/16/china-gebruikt-nieuwe-zijderoute-om-politieke-invloed-te-krijgen/?gdpr=accept; https://www.geotrendlines.nl/china-investeert-miljoenen-in-griekse-haven/

(17)https://www.theguardian.com/commentisfree/2019/nov/29/mass-consumerism-black-friday-climate-catastrophe-consumption-shopping; https://newrepublic.com/article/154147/climate-change-symptom-consumer-culture-disease;

https://www.ucgroup.nl/willglobalsupplychainsbecomeobsolete/

Deel dit artikel: